:strip_icc():format(webp)/kly-media-production/medias/5082523/original/082651200_1736234619-patrick.jpg)

Understanding the Fees and Costs Associated with SBA Real Estate Loans

Discover the fees and costs associated with SBA real estate loans, including closing costs, guarantee fees, appraisal expenses, and more. Learn what to expect and how to budget effectively.

Small Business Administration (SBA) loans are a valuable financing option for business owners looking to acquire commercial real estate. However, understanding the various fees and costs associated with these loans is crucial for effective financial planning. If you're considering an SBA real estate loan in Chesapeake, VA, this guide will help you break down the expenses involved and how they impact your total loan cost.

Key Fees and Costs of SBA Real Estate Loans

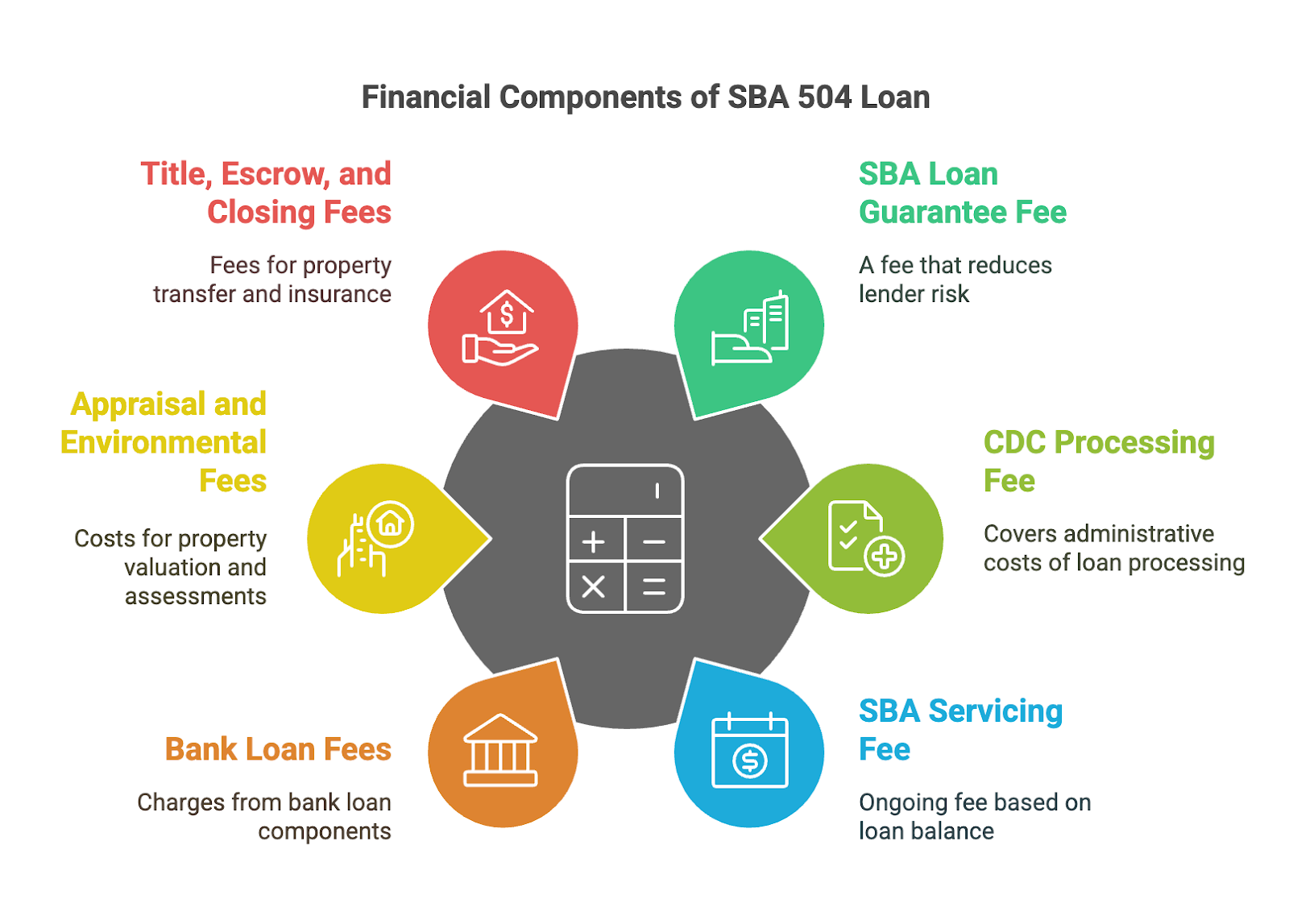

When applying for an SBA 504 loan, business owners must account for various fees and costs that impact the total expense of financing. While SBA loans offer lower down payments, longer terms, and competitive interest rates, understanding the breakdown of associated fees ensures transparency and better financial planning. Below are the key expenses to consider when securing an SBA real estate loan.

1. SBA Loan Guarantee Fee

The SBA loan guarantee fee is a mandatory cost applied to all SBA-backed loans to help cover the agency’s expenses in guaranteeing the loan. Since the SBA does not lend money directly, it assumes part of the lender’s risk by guaranteeing a portion of the loan. In exchange for this guarantee, borrowers pay a fee ranging from 2% to 3.5% of the guaranteed portion of the loan amount.

-

The exact fee percentage depends on the total loan amount and repayment term.

-

It is usually financed into the loan, meaning borrowers can roll this cost into their total loan balance rather than paying upfront.

-

Since this fee is non-refundable, it is important to factor it into the total cost before proceeding with a loan application.

For businesses seeking large financing amounts, the guarantee fee can be a substantial cost, but it enables lenders to approve loans with lower interest rates and longer repayment terms compared to conventional financing.

2. CDC Processing Fee

Certified Development Companies (CDCs), such as 504 Capital, serve as intermediaries between lenders and borrowers, ensuring that SBA 504 loans are properly structured, processed, and serviced. To cover administrative costs, CDCs charge a processing fee of 1.5% of the total loan amount.

-

This fee is typically financed as part of the loan and paid at closing.

-

It covers essential services such as application review, loan structuring, underwriting, and compliance checks.

-

Borrowers benefit from the CDC’s expertise, ensuring smooth loan approval and compliance with SBA regulations.

Since SBA 504 loans have longer repayment terms and fixed interest rates, this processing fee is a one-time expense that contributes to securing favorable loan terms for small businesses.

3. SBA Servicing Fee

The SBA servicing fee is an ongoing cost that applies for the entire duration of the loan. This fee is charged annually as a percentage of the outstanding principal balance, typically ranging from 0.3205% to 0.4517% per year.

-

The servicing fee helps cover administrative costs associated with maintaining the loan, such as compliance monitoring, payment processing, and SBA oversight.

-

Borrowers should factor in this fee when calculating their effective loan interest rate.

-

Since it is applied annually, the total amount paid depends on how long the loan remains active.

While this fee may seem small, it adds up over the life of the loan and contributes to the overall borrowing cost.

4. Bank Loan Fees

SBA 504 loans are structured in two parts:

-

50% of the loan amount comes from a traditional lender (such as a bank or credit union).

-

40% comes from the SBA-backed CDC loan.

-

The remaining 10% is the borrower’s down payment.

Since traditional banks are involved in financing half of the SBA 504 loan, they may charge additional fees such as:

-

Origination fees (typically 0.5%–1% of the loan amount).

-

Underwriting fees, which cover the lender’s cost of evaluating the borrower’s creditworthiness.

-

Administrative and documentation fees for processing loan paperwork.

These fees vary from lender to lender, so it’s important to compare options when selecting a financing partner.

5. Appraisal and Environmental Fees

Before approving an SBA real estate loan, lenders require property appraisals and environmental assessments to determine the value and potential risks of the financed property.

-

Appraisal fees range from $2,000 to $5,000, depending on the complexity and size of the commercial property.

-

Environmental assessments (such as Phase I or Phase II Environmental Site Assessments) may be required to identify potential contamination or hazards. These cost $1,500 to $3,000 on average.

If a property has environmental concerns, further testing or remediation may be needed, increasing costs significantly. Business owners purchasing older properties, industrial sites, or locations with known environmental risks should budget for additional due diligence expenses.

6. Title, Escrow, and Closing Fees

Securing an SBA loan requires proper legal documentation and ownership verification, which adds title, escrow, and closing costs to the total loan expense.

-

Title insurance protects the lender and borrower from ownership disputes or legal claims against the property.

-

Escrow fees cover the costs of a third-party escrow service managing fund transfers, closing statements, and compliance checks.

-

Closing fees (including recording fees, wire transfer fees, and legal documentation costs) typically range from $2,000 to $4,000.

These fees are paid at closing and vary depending on the location and complexity of the transaction.

7. Legal Fees

While not always mandatory, some SBA real estate loan transactions require legal representation to review and draft financing documents.

-

Legal fees can range from $2,500 to $5,000, depending on the complexity of the transaction.

-

If the loan involves multiple properties, partnerships, or additional collateral, legal costs may be higher.

-

Borrowers should consult their lender to determine whether legal review is necessary for their loan application.

Some business owners choose to hire an attorney specializing in SBA loans to ensure compliance and safeguard their interests, which may add further legal costs.

8. Prepayment Penalties

SBA loans are designed for long-term financing, and early repayment may result in prepayment penalties. These penalties are in place to prevent borrowers from paying off the loan too soon, as SBA-backed lenders rely on long-term interest payments for profitability.

-

Prepayment penalties typically apply within the first 10 years of the loan term.

-

The fee follows a declining scale, meaning the penalty percentage decreases each year.

-

The penalty is calculated based on the outstanding principal balance at the time of prepayment.

For borrowers who plan to refinance or pay off their loan early, understanding prepayment penalties is crucial. Discussing these terms upfront with 504 Capital ensures transparency and helps businesses plan their repayment strategy.

Why Choose an SBA 504 Loan Through 504 Capital?

At 504 Capital, we specialize in SBA loans in Chesapeake, VA, helping business owners secure competitive financing with low interest rates and flexible repayment terms. Our experienced team guides you through every step, from application to closing, ensuring a seamless loan process.

Benefits of choosing 504 Capital:

✅ Lower Down Payments – Only 10% required, unlike traditional loans that demand 20%-30%.

✅ Fixed Interest Rates – No balloon payments or unexpected rate hikes.

✅ Longer Loan Terms – Up to 25 years, reducing monthly payments.

✅ Larger Loan Amounts – Borrow up to $20 million for real estate projects.

✅ Expert Loan Support – We handle the paperwork and streamline the process.

Final Thoughts

Understanding the costs of SBA real estate loans is crucial before applying. While SBA loan fees add to the total expense, the benefits often outweigh the costs, making it a smart choice for small business owners looking to grow.

If you're ready to invest in commercial real estate, 504 Capital is here to help. Contact us today to explore SBA loans in Chesapeake, VA, and secure financing that supports your business goals.

Call us or apply online to get started.

What's Your Reaction?